Based on 3 new benchmarking reports, here are the key trends shaping the SaaS market in 2024.

3 new benchmarking reports dropped on the state of SaaS in the first half of 2024.

We had Ebsta’s ' B2B Sales Benchmarks ', ChartMogul’s ‘ Market Insights ’ and DreamData’s ‘ 8 B2B Benchmarks (3rd Edition) ’.

Overall they paint a picture of the SaaS industry continuing to face challenges in 2024, with growth rates remaining sluggish throughout the first half of the year.

However, amidst these difficulties, some segments show signs of improvement, and companies are adapting their go-to-market strategies to navigate the changing landscape.

Here are the key trends shaping the SaaS market in 2024.

1. Persistent Slow Growth

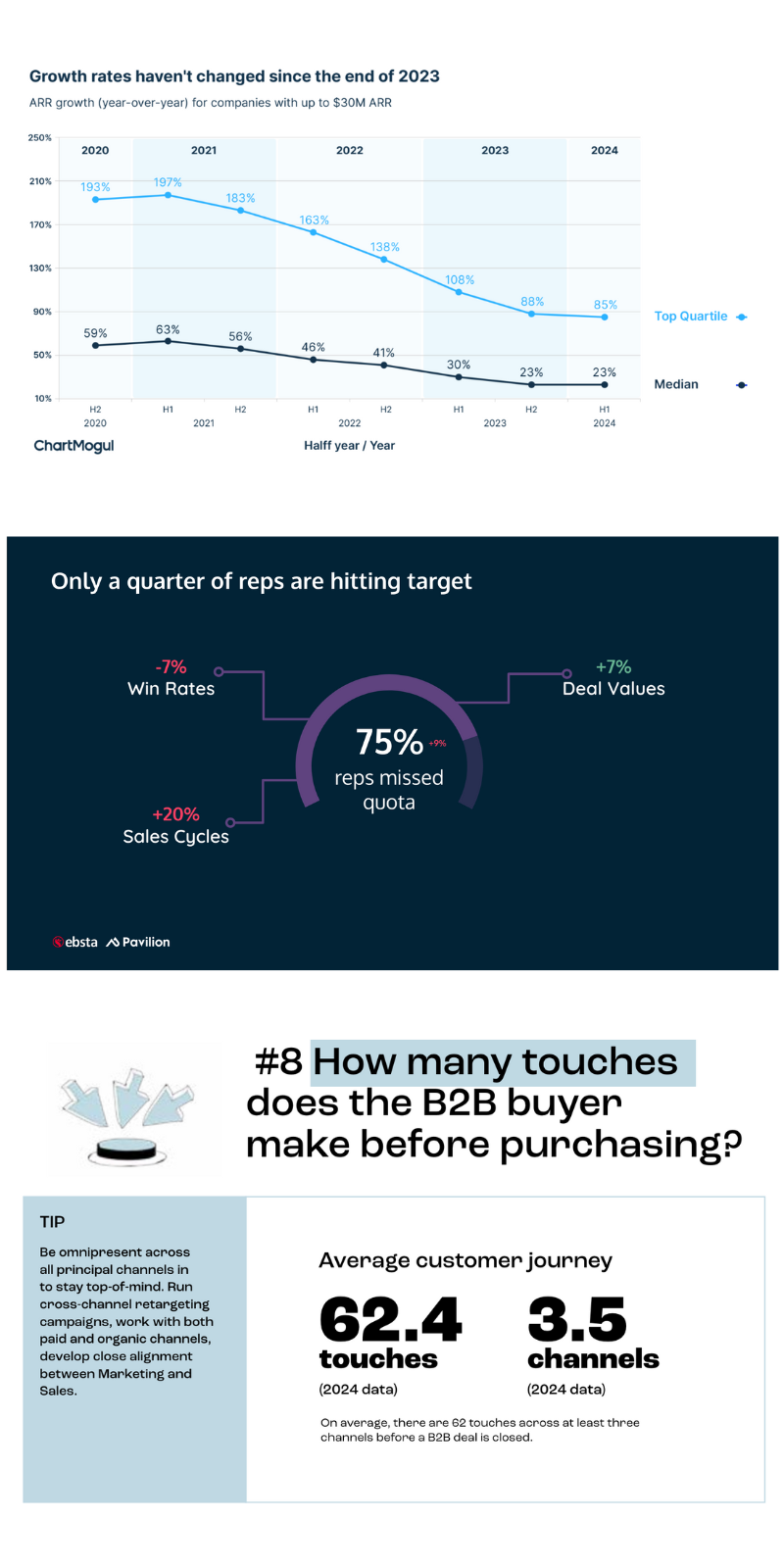

The overall growth rate for SaaS companies has remained relatively stagnant, with the median Annual Recurring Revenue (ARR) growth rate holding steady at 23% in June 2024, unchanged from the end of 2023.

This trend indicates that the industry is still grappling with the aftermath of the economic downturn experienced in recent years.

It also shows that overall, most businesses haven’t figured out a new GTM model yet. Too many are still executing the old playbooks, which simply don’t work now.

2. Segment-Specific Growth Improvements

While overall growth remains slow, certain segments are showing signs of recovery:

- Companies with Average Revenue Per Account (ARPA) over $1,000 saw a 4 percentage point improvement, reaching 45% growth.

- The $250-500 ARPA segment also grew by 4 percentage points, hitting 26% in June.

- SaaS companies in the $8-15M ARR range showed a 5 percentage point improvement, with a median growth rate of 29%.

These pockets of growth offer a glimmer of hope for the industry, suggesting that some segments are beginning to recover.

3. Longer Sales Cycles and Complex Buying Journeys

The B2B customer journey in SaaS has become increasingly complex.

On average, it takes 192 days from the first touch to a closed deal, with larger companies (>250 employees) experiencing 65% longer journeys compared to smaller ones. This extended sales cycle highlights the need for patience and strategic planning in go-to-market efforts.

4. Multi-Stakeholder Involvement

B2B buying decisions are increasingly made by committee, with an average of 6.3 stakeholders involved in each deal.

This trend underscores the importance of tailoring marketing and sales activities to address the needs and concerns of multiple decision-makers, not just end-users.

5. Shift Towards Self-Serve Research

A significant portion (83%) of the B2B buyer journey now occurs without direct seller involvement.

This shift really highlights the need for comprehensive self-serve content and strong social proof across all relevant channels.

It’s not a strong competency build out for most mid-market to enterprise go-to-market teams in B2B SaaS, and I think it presents a huge pocket of opportunity for those willing to embrace a more educational, less transactional approach to customer growth.

6. Importance of Qualification and Discovery

Top-performing sales teams are placing greater emphasis on effective qualification and discovery processes.

Companies that match opportunities with their Ideal Customer Profile (ICP) see a 3.1x increase in win rates.

Additionally, adoption of qualification methodologies has increased by 19% since 2023.

This is still a weak spot though. Even as pipeline value has increased significantly, rep attainment has continued to drop (to just 25%!), which shows many organisations are not generating the right opportunities.

7. Multi-Channel Engagement

On average, B2B buyers make 62.4 touches across at least 3.5 channels before making a purchase.

This highlights the importance of maintaining an omnichannel presence and developing cross-channel retargeting campaigns.

8. Focus on Customer Retention

With growth rates declining, many SaaS companies are focusing on retention as a key driver of growth.

Net Revenue Retention (NRR) has become a critical metric, with top performers in higher ARPA segments maintaining 100% NRR despite challenging market conditions.

9. Increased Scrutiny on ROI and Value

Buyers are becoming more discerning in their investment decisions. Objections concerning ROI and value have increased by 127% since 2023, while concerns about functionality (including AI features) have risen by 111%.

This trend underscores the need for clear value propositions and robust ROI justifications in sales processes.

It also shows that you can’t simply rely on sales and marketing leaders to continuously pull rabbits out of their hat - product and engineer teams have to keep up with the pace of innovation of deliver solutions that genuinely deliver value.

10. Adoption of AI and Data-Driven Strategies

To adapt to these challenging market conditions, many SaaS companies are leveraging AI and data-driven approaches to improve their go-to-market strategies.

This includes using AI for pipeline visibility, objection handling, and relationship scoring to improve multi-threading in complex deals.

We’re also excited by the potential for AI to help vendors move to a more Value-Led Sales motion, allowing them to engage the whole market and build both pipeline and brand reputation through delivering consistently relevant content to prospects.

Conclusion

The SaaS market in 2024 presents a mixed picture of persistent challenges and emerging opportunities.

While overall growth remains slow, certain segments are showing signs of recovery.

To succeed in this environment, SaaS companies must adapt their go-to-market strategies to address longer sales cycles, multi-stakeholder decision-making, and increased buyer scrutiny.

By focusing on adding value, effective qualification, leveraging data-driven insights, and maintaining a strong

multi-channel presence, SaaS businesses can position themselves for growth even in these challenging times.